Zebra Technologies Unveils CV70 Camera, Eyes Software Growth

The automation vendor is pairing new machine vision hardware with integrated software to chase higher-margin recurring revenue, but hardware dependence and tariff exposure remain risks.

Zebra Technologies introduced its ultra-compact CV70 CXP machine vision camera at Automate 2026 earlier this month, part of an expanded automation portfolio that spans RFID, industrial scanning, and workflow optimization tools designed to cover manufacturing operations from raw materials to final distribution.

The launch signals Zebra's strategic shift toward integrated, single-vendor automation systems that combine hardware like the CV70 with its Aurora software, vision controllers, and RFID-enabled factory infrastructure. The goal is to offer manufacturers improved asset visibility, quality control, and intelligent automation through tightly coupled hardware-software bundles.

Why it matters

Zebra's move to pair high-performance machine vision cameras with orchestration and analytics software addresses a critical question for investors: can the company transition from hardware-centric revenue to higher-margin recurring software and services income? Success would reduce exposure to competitive hardware cycles and improve earnings quality, but the company remains vulnerable to tariff-related cost pressures and hardware dependence if software adoption lags.

The software integration play

The CV70 launch builds on Zebra's June introduction of Zebra Nucleus and expanded Workcloud software, which provide orchestration, analytics, and integration capabilities across the company's device ecosystem. This hardware-software pairing directly targets the catalyst of growing recurring revenue, but execution risk remains if software pricing or adoption fails to meet expectations.

Analysts project Zebra will reach $6.7 billion in revenue and $819.8 million in earnings by 2029, requiring 7.5 percent annual revenue growth and a $400.8 million increase in earnings from the current $419.0 million baseline. However, more cautious analysts forecast revenue of approximately $6.6 billion and earnings near $665 million by 2029, reflecting divergent views on how automation demand and tariff risks will play out.

Investment considerations

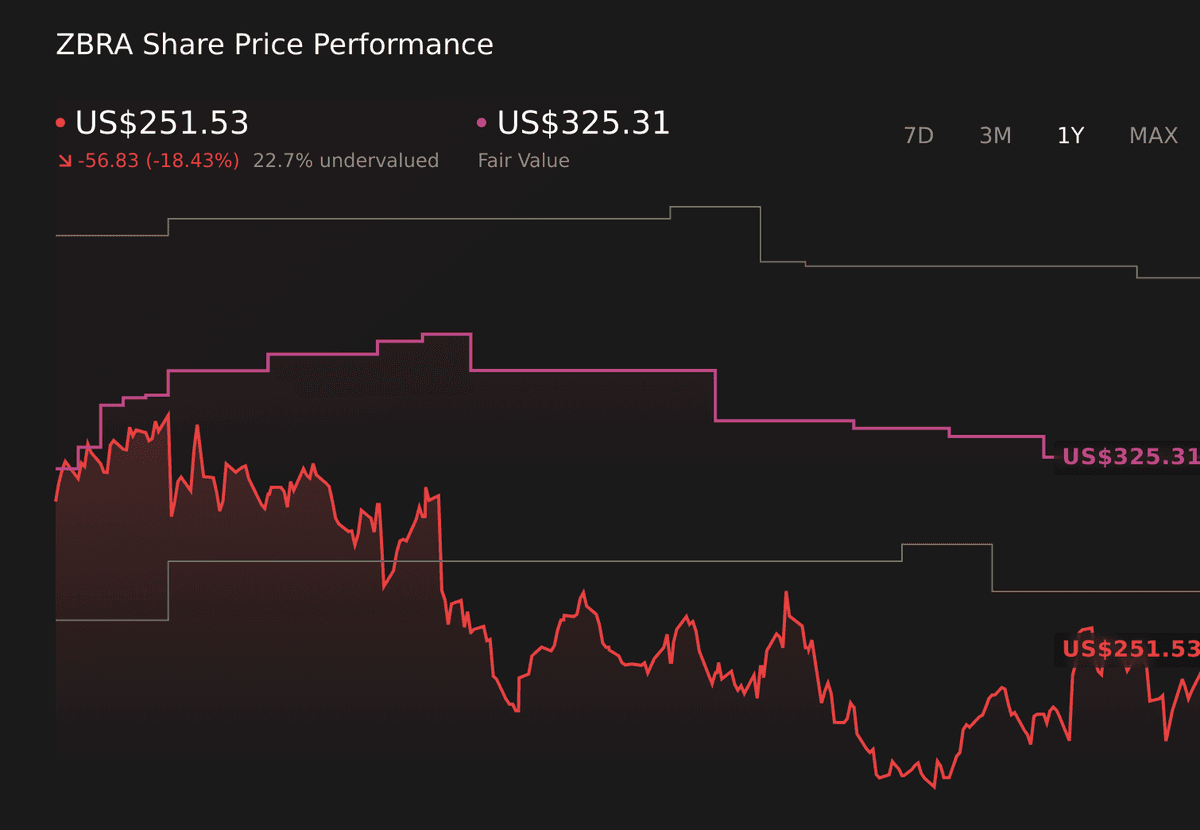

Zebra's investment thesis hinges on its ability to position itself at the center of integrated automation systems where hardware, software, and data capture function as a unified platform. The company's fair value has been estimated at $325.31 by some analysts, representing a 29 percent upside to current prices, though valuations vary widely based on assumptions about software adoption rates and margin expansion.

The primary risk remains that despite automation tailwinds, Zebra could stay more exposed to hardware commoditization and tariff-driven cost pressures than investors anticipate if the software transition moves slowly.

These details were first reported by Simply Wall St.

This is an original analysis by the Omega editorial team. Source reporting: Automation Watch.

Want systems like this working for your business?

Book a Call