SK hynix Hits $1 Trillion Valuation on Nvidia HBM4 Orders

The Korean memory maker is expanding fabrication capacity to meet surging demand for high-bandwidth memory in AI accelerators.

SK hynix Reaches Trillion-Dollar Milestone

SK hynix has crossed the $1 trillion market capitalization threshold, driven by its strategic position as a supplier of high-bandwidth memory (HBM) for artificial intelligence hardware. The Korean semiconductor manufacturer has secured significant HBM4 supply orders from Nvidia, cementing its role in the AI accelerator supply chain.

According to Yahoo Finance, which first reported these details, the company is now investing heavily in new fabrication capacity to support both HBM and DRAM production. These long-term contracts and capacity expansions are designed to provide more stable supply for AI and data center customers as demand for advanced memory solutions intensifies.

Why it matters

HBM4 represents the next generation of memory technology essential for training and running large AI models. SK hynix's ability to secure major orders from Nvidia—the dominant player in AI chips—positions it as a critical infrastructure provider in the AI boom. However, the company's customer concentration and massive capital expenditure requirements introduce execution risk that investors must weigh against the growth opportunity.

Valuation and Market Dynamics

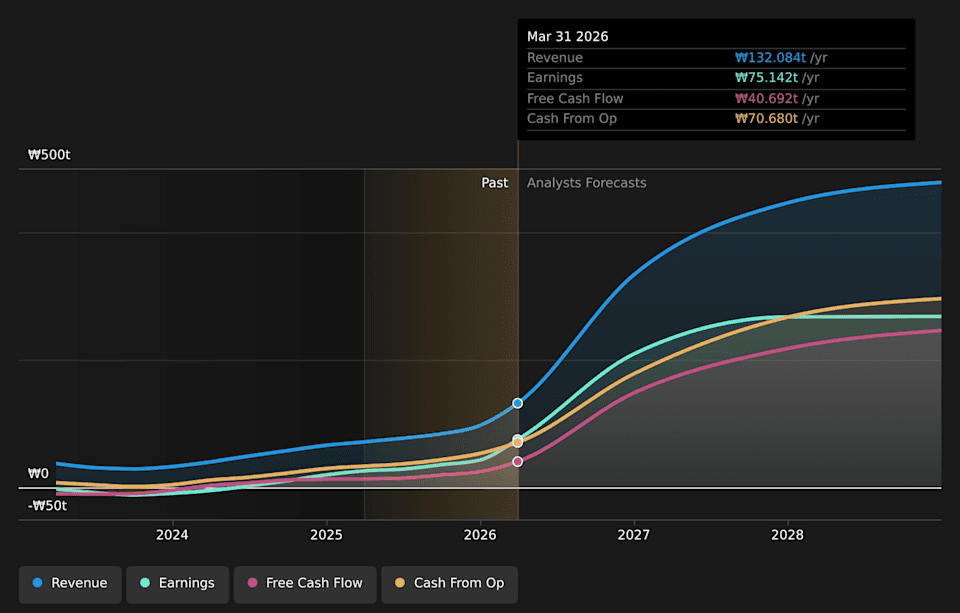

SK hynix shares currently trade at ₩2,360,000, approximately 25% above the analyst consensus target of ₩2,076,603. The stock has surged 63.1% over the past 30 days, reflecting investor enthusiasm around AI memory demand and capacity expansion plans.

Despite trading above analyst targets, some valuation models flag the shares as undervalued—trading 46.2% below one estimate of fair value. The company's price-to-earnings ratio stands at 22.2, modestly below the industry average of 24.4.

Investment Considerations

The HBM4 orders from Nvidia reinforce SK hynix's central role in AI memory infrastructure, but several factors warrant attention. The company is undertaking a substantial capital expenditure program to build new fabrication facilities, which will affect near-term margins and require careful monitoring of return on investment.

One flagged risk involves high non-cash earnings, suggesting investors should track cash conversion rates to ensure reported profit quality aligns with headline growth figures. The wide analyst target range—from ₩1,030,000 to ₩4,000,000—reflects significant uncertainty about how capacity investments, pricing power, and customer concentration will shape the company's risk-reward profile over time.

As HBM becomes increasingly critical for high-performance computing workloads, SK hynix's ability to execute on capacity expansion while maintaining profitability will determine whether the current valuation proves sustainable.

These details were first reported by Yahoo Finance.

This is an original analysis by the Omega editorial team. Source reporting: AI Watch.

Want systems like this working for your business?

Book a Call