Honeywell to Split Aerospace and Automation Into Separate Companies

The industrial conglomerate will spin off its aerospace division under activist pressure, creating two distinct investment vehicles.

Honeywell International is moving forward with plans to separate its aerospace operations from its automation business, creating two independent publicly traded companies in response to activist investor pressure.

The conglomerate will spin off Honeywell Aerospace as a dedicated aerospace pure-play entity, while the remaining operations will rebrand as Honeywell Technologies with a focus on automation and related solutions. The transaction is described as imminent, though formal timing, transaction terms, and capital structure details have not yet been disclosed.

Why it matters

The separation allows investors to choose between two distinct exposure profiles rather than holding a diversified conglomerate. Aerospace and automation businesses face different cyclical patterns, regulatory environments, and capital requirements. By splitting them, each company can pursue sector-specific strategies and be valued against more comparable peers. The move also reflects broader market pressure on industrial conglomerates to simplify their structures and unlock shareholder value.

What changes for investors

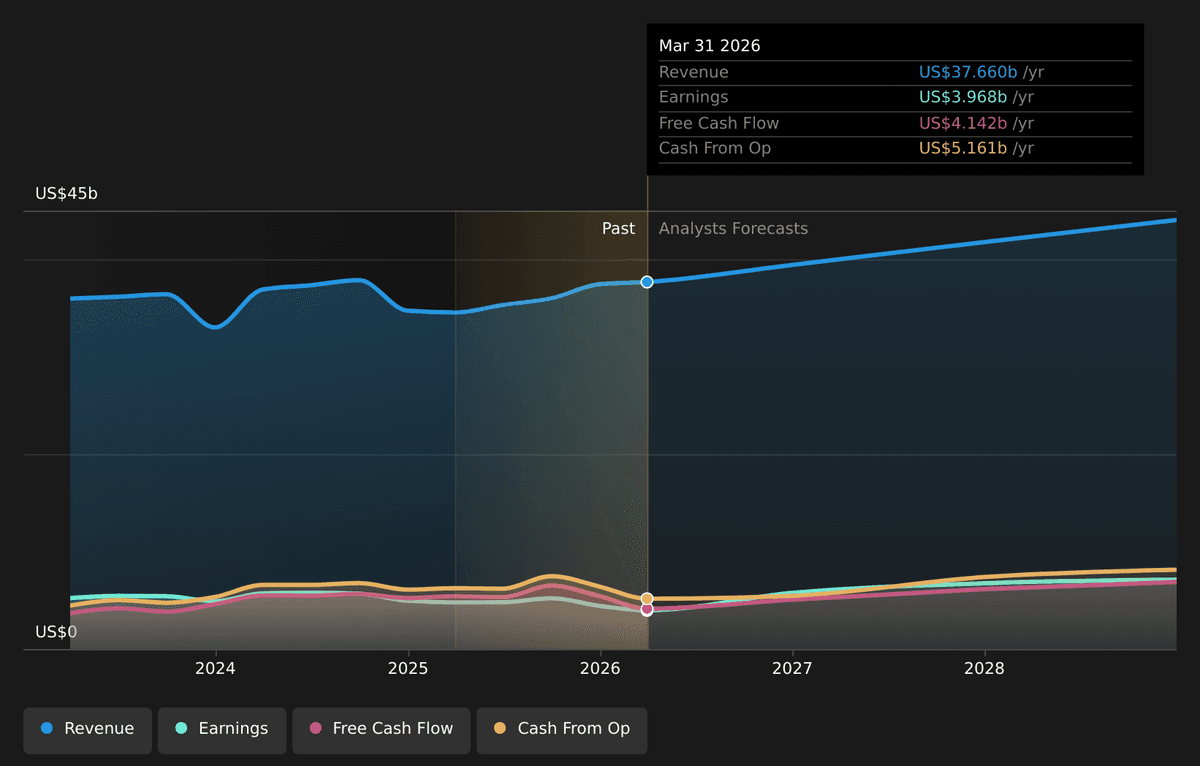

The restructuring fundamentally alters how Honeywell's business mix is grouped and reported. Currently trading at $215.70—approximately 13% below the analyst price target of $247.82—the stock has gained 1.2% over the past 30 days as the spin-off approaches.

Once separated, each entity will establish independent capital allocation priorities, cost structures, and dividend policies. Investors will need to evaluate governance decisions, balance sheet strength, and management priorities for both companies separately. The current analyst target range of $198 to $292 will likely be revised once each company's financial structure becomes clear.

Outstanding questions

Key details remain unresolved. How will existing debt be allocated between the two entities? One concern flagged in current analysis is that Honeywell's debt is not well covered by operating cash flow, making leverage and interest coverage important metrics to monitor post-separation.

Dividend policy represents another critical unknown. Will both companies maintain payouts, or will one prioritize reinvestment? How price-to-earnings ratios settle for each entity will influence their relative appeal to different investor segments.

The separation follows pressure from activist investors seeking to unlock value in what they view as an undervalued conglomerate structure. Whether the sum of the parts proves greater than the whole will depend on execution details that have yet to be announced.

These details were first reported by Simply Wall St.

This is an original analysis by the Omega editorial team. Source reporting: Automation Watch.

Want systems like this working for your business?

Book a Call