US Industrial Robot Installations Return to Double-Digit Growth

Food sector automation surged 30% as robot density climbed to 307 units per 10,000 workers, placing America eighth globally.

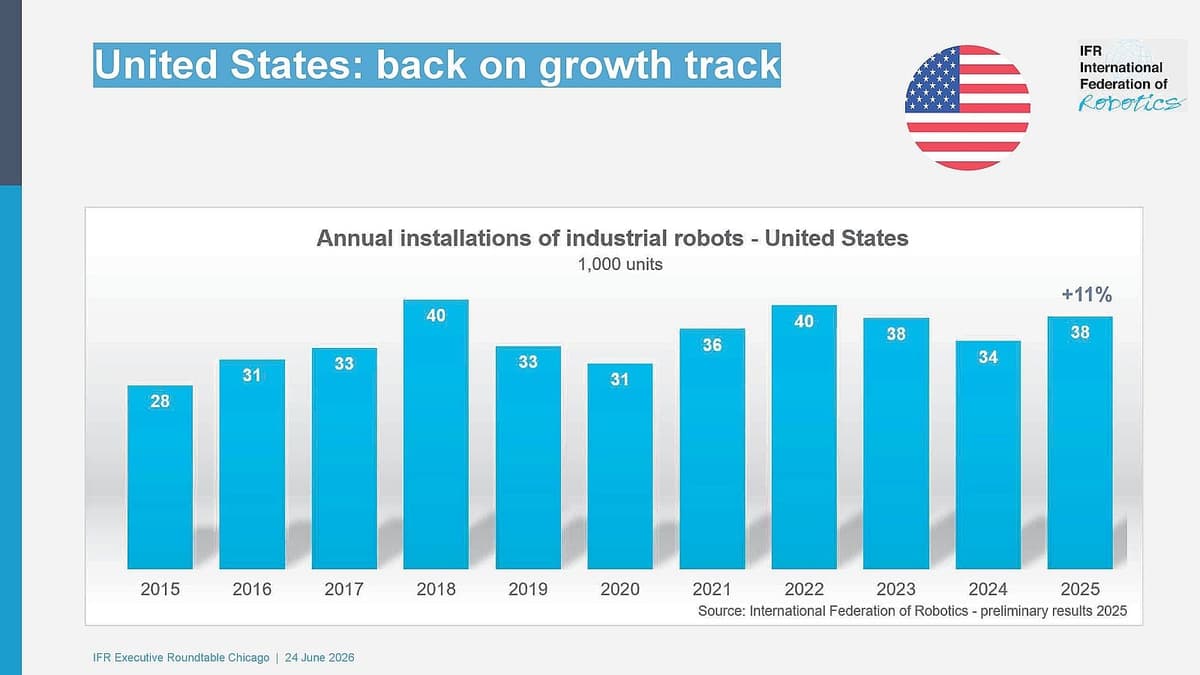

US Automation Sector Rebounds with Broad-Based Growth

The United States industrial robotics market has returned to double-digit growth, driven by diversifying demand beyond traditional automotive applications, according to the International Federation of Robotics. While automotive manufacturing posted its third-strongest performance in seven years, the food industry emerged as a standout sector with installations surging 30% to reach approximately 3,000 units in 2025.

The food sector now ranks alongside metal and machinery and electrical-electronics in total installations, signaling a shift toward flexible automation in industries historically slower to adopt robotics technology.

Robot Density Places US Eighth Globally

The US achieved a robot density of 307 industrial robots per 10,000 manufacturing employees, advancing two positions to eighth place worldwide. This metric trails automation leaders South Korea (1,220 robots per 10,000 workers), Germany (449), and Japan (446), but exceeds China's density of 166 robots per 10,000 employees.

Despite lower density, China dominates in absolute volume. The country installed 295,000 units in 2024, capturing 54% of the global market. IFR estimates Chinese installations in 2025 were roughly ten times higher than US figures, a result of China's decade-old national robotics strategy. The country's 15th Five-Year Plan (2026–2030) positions robotics as central to its industrial modernization, with AI research focused on physical applications to drive economic growth.

Industry Group Proposes Federal Robotics Strategy

A3, North America's largest automation trade association, has published a "Vision for a National Robotics Strategy" and presented it to lawmakers. The framework calls for establishing a Federal Robotics Office and National Commission to coordinate policy and harmonize government research through public-private partnerships.

The proposed strategy includes market-driven tax incentives, expanded workforce retraining programs, updated safety standards, and federal procurement mandates for domestic robotics technology to accelerate commercial deployment.

Why It Matters

The US faces a structural challenge: China's coordinated national strategy has produced installation volumes an order of magnitude larger, creating economies of scale in robotics development and manufacturing. Without comparable federal coordination, American manufacturers risk falling further behind in automation capabilities despite strong near-term growth. The proposed national strategy represents an attempt to address this competitive gap through policy rather than market forces alone.

Outlook Remains Positive Despite Competition

IFR projects continued long-term growth for North American automation, driven by factory reshoring initiatives and persistent skilled labor shortages. Manufacturers are increasing automation investments to address structural workforce gaps as demand spreads beyond traditional sectors.

These details were first reported by the International Federation of Robotics. IFR Vice President Jane Heffner will present preliminary 2026 North American installation figures at the Automate Show in Chicago on June 24.

This is an original analysis by the Omega editorial team. Source reporting: Automation Watch.

Want systems like this working for your business?

Book a Call